Key takeaways

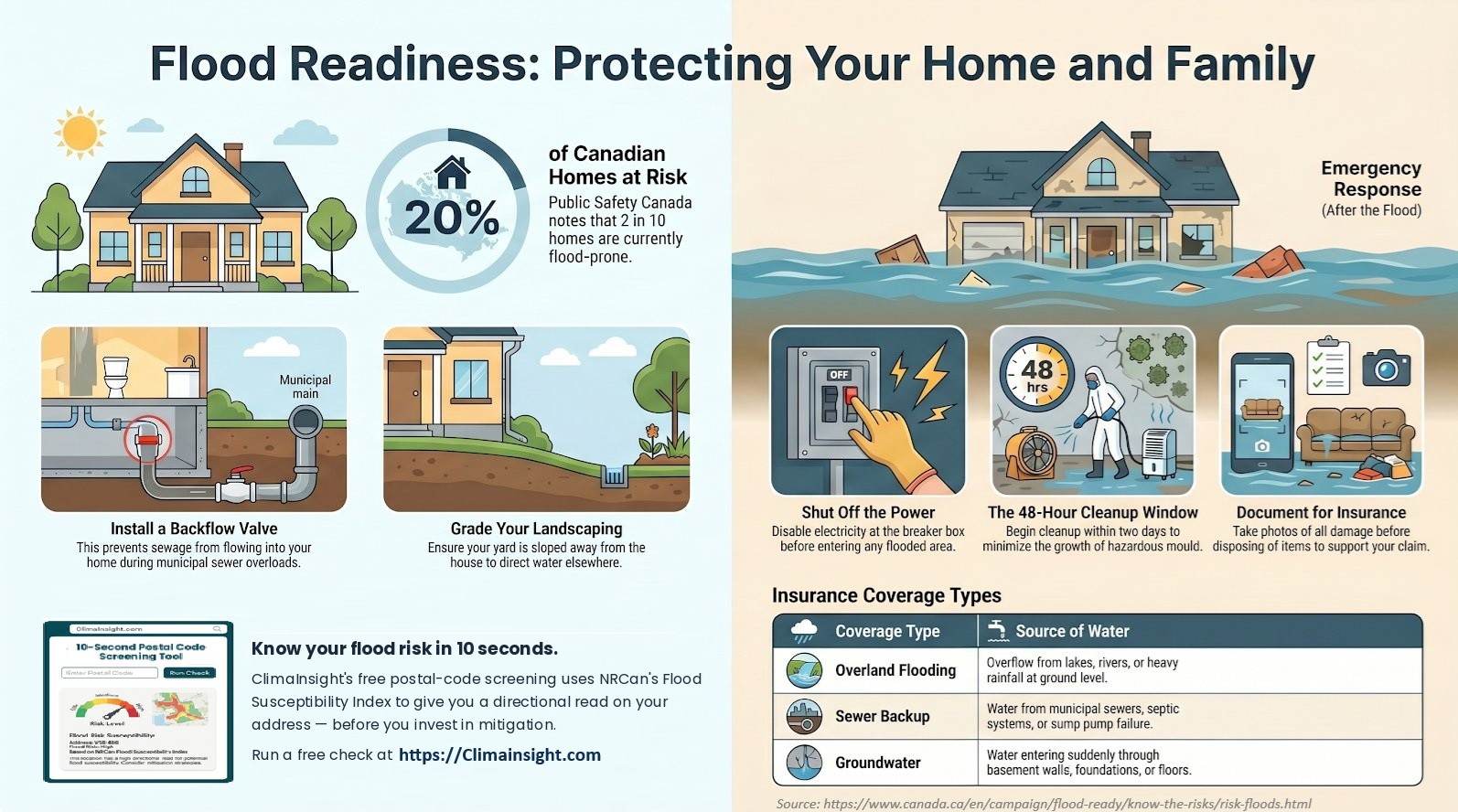

- Public Safety Canada estimates that roughly 1 in 5 Canadian homes is flood-prone — and flooding is the most common and costly natural hazard in the country.

- Two low-cost mitigation measures — a backflow valve and proper lot grading — prevent a large share of residential flood damage.

- After a flood, the first hours matter: cut the power, start cleanup within 48 hours, and document everything before you throw it out.

- Standard home insurance does not automatically cover all water damage. Overland flooding, sewer backup, and groundwater seepage are three separate coverages — confirm which ones you actually hold.

The scale of the risk

Flooding is Canada's most frequent and most expensive natural hazard, with average annual losses exceeding $2 billion. Public Safety Canada notes that approximately 2 in 10 homes sit in flood-prone areas. Spring melt, intense rainfall, and aging municipal stormwater systems all push that number in the wrong direction.

The encouraging part: a meaningful share of residential flood damage is preventable, and the rest is far cheaper to recover from if you have a plan before the water arrives.

Before the flood: two measures worth the cost

Install a backflow valve

During heavy rain, municipal sewer mains can overload and reverse — pushing sewage back up the line and into the lowest drains in your home. A backflow valve (also called a backwater valve) closes automatically when flow reverses, blocking that sewage from entering. Many municipalities offer subsidy programs to offset the installation cost. For a basement-finished home, it is one of the highest-return mitigation investments available.

Grade your landscaping away from the house

Water follows the slope of the ground. If your lot grades toward the foundation, every rainfall drains against your basement walls. The fix is straightforward: ensure the soil within roughly two metres of the house slopes away from it, and keep downspout extensions directing roof runoff well clear of the foundation. This costs little and protects against groundwater seepage — the hardest flood type to insure against.

After the flood: the first 48 hours

Shut off the power

Before entering any flooded area, disable the electricity at the breaker box — and only do so if you can reach the panel without standing in water. Energized water is a lethal hazard. If the panel itself is wet or unreachable, call your utility or an electrician.

Treat the 48-hour cleanup window seriously

Mould begins to establish within 24 to 48 hours of materials getting wet. Begin removing standing water, wet drywall, insulation, and saturated contents as quickly as it is safe to do so. Acting inside that window is the single biggest factor in whether a flooded basement becomes a cleanup or a gut renovation.

Document everything before you discard it

Insurers need evidence. Photograph all damage — structure, finishes, and contents — before you dispose of anything. Record serial numbers where you can, and keep receipts for emergency repairs and accommodation. A thorough photo record is what turns a contested claim into a paid one.

Know your coverage: flood is not one thing

A common and costly misunderstanding is assuming a standard home policy covers "flooding." In Canada, water damage is split across three distinct coverages, and you may hold some, all, or none of them:

| Coverage type | Source of water |

|---|---|

| Overland flooding | Overflow from lakes, rivers, or heavy rainfall pooling at ground level. |

| Sewer backup | Water from municipal sewers, septic systems, or sump pump failure. |

| Groundwater | Water entering through basement walls, foundations, or floors. |

Overland flood coverage is often an optional add-on, and groundwater seepage is frequently excluded entirely. Call your broker and confirm in writing which of the three you carry — before you need them, not after.

Start with a 10-second screen

You can't plan around a risk you haven't measured. Knowing whether your address sits in a higher-susceptibility area tells you how much of the checklist above is urgent versus precautionary.

ClimaInsight's free postal-code screening uses NRCan's Flood Susceptibility Index to give you a directional read on your property in about ten seconds — before you invest in mitigation or shop for coverage. Run a free check at climainsight.com.

It's a starting point, not a substitute for the federal Flood Risk Finder or a professional assessment — but it's a fast, no-cost way to know where your home stands today.

Sources: Public Safety Canada — Flood Ready; Insurance Bureau of Canada flood coverage guidance.